Wollert Rise: First Home Buyers Seminar.

Wollert Rise: First Home Buyers Seminar

Buying your first home is one of the biggest decisions you’ll ever make. That’s why the team at Wollert Rise recently brought together a panel of experts to demystify the journey for first home buyers, from understanding your borrowing capacity to navigating contracts, government incentives and everything in between.

The seminar covered the practical, financial and legal realities of purchasing land and building a home. Whether you attended on the day or are just beginning to explore the path to home ownership, this recap pulls together the key takeaways so you can enter the property market with confidence. You can watch the full seminar below:

Key takeouts from the seminar

Borrowing Capacity Isn’t the Same as Affordability

One of the most common mistakes first home buyers make is treating the maximum a lender is willing to lend as the amount they should spend. Lenders look at your income, expenses, liabilities and repayment capacity. They’ll assess your verifiable income: think payslips or BAS statements if you’re self-employed along with a clean credit history and minimal existing debt.

A larger deposit doesn’t necessarily increase your borrowing power either, what matters most is your cashflow and ability to meet repayments. Affordability is a separate question. It’s about what you feel comfortable repaying each month, factoring in your lifestyle and financial goals. Setting that number before you start looking, and sticking to it, can make all the difference.

Understanding the Home Loan Journey

Applying for a home loan for the first time can feel overwhelming, but it’s much more manageable when you know what to expect.

To start the process, we’d recommend gathering all your financial information like ID, statements and payslips, then we’ll submit your loan application to the lender. From there, the lender reviews your application with the verifying documents and issues your pre-approval or conditional approval. This is where the bank checks if certain conditions are met. Most pre-approvals follow the 90/90 rule: valid for 90 days, with some lenders giving you the option to extend for another 90.

Once the outstanding conditions are met, you’ll move to formal approval – the binding and unconditional stage. After that, your loan contract is issued, and the final step is settlement: the exchange of funds and the transfer of land in your name. This is the moment you’ve been waiting for! The biggest thing to remember is a little preparation goes a long way. Having your documents ready from the start helps avoid delays, keeps your application moving forwards and means fewer surprises along the way.

Make the Most of First Home Buyer Assistance

The good news for first home buyers? There’s financial support available to help you move into your new home sooner. In Victoria, you may be able to access the First Home Owner Grant, a $10,000 payment to help you buy or build a new home. It applies to newly constructed or never-occupied properties valued at $750,000. Stamp duty is also abolished for first home buyers purchasing a property for $600,000 or less, with reduced rates available up to $750,000 – visit the State Revenue Office for more information.

On top of that, the Australian Government’s Deposit Scheme allows first home buyers to purchase a property with just a 5% deposit, or as little as 2% for single parents. If you don’t quite fit the criteria, there are other pathways worth exploring like guarantor arrangements or equity-based solutions. Eligibility criteria vary across each scheme, so it’s worth checking what you qualify for early in the process and factoring it into your bigger financial picture.

The Hidden Costs Buyers Need to Budget For

Buying land involves more than just the advertised price, and knowing the full costs upfront makes budgeting a whole lot easier. There are a handful of extra costs to be aware of along the way: things like stamp duty (where it applies), title registration fees, legal and conveyancing costs or building and other settlement-related expenses. Careful budgeting at the start helps avoid unexpected financial pressure further down the line.

Understanding the Contract Process

Buying off-the-plan follows a slightly different path to buying an established home. The key stages to know are: making an offer, signing the contract, obtaining finance approval, registration of the plan of subdivision and finally settlement. One thing worth keeping in mind is that settlement timing can be affected by subdivision registration and other project milestones, so it’s worth leaving a little room for flexibility in your timeline.

Common Risks First Home Buyers Should Watch For

Not sure what to look for as a first home buyer? There are a few things worth noting as you move through the process. From understanding your finance conditions and the cooling-off periods, to allowing for potential delays in subdivision registration, these are some of the common pitfalls we raised during the seminar.

It’s also worth paying close attention to construction commencement and completion requirements, along with any easements, covenants or design guidelines that could shape what you’re able to build. Lastly, making sure you’ve accounted for all the costs payable at settlement is incredibly important. None of this should stand in the way of your purchase, it simply makes the process easier to manage when you know what to look out for.

Why Professional Advice Matters

You don’t have to navigate the buying process on your own. That’s where a property lawyer brings the most value. They can review contracts before you sign, flag any title restrictions or easements that could affect your land, keep track of key deadlines along the way and help you sidestep the kind of costly mistakes that can be hard to spot as a first home buyer. Having this extra layer of guidance, particularly for first home buyers purchasing off-the-plan, can reduce the risk and bring you real peace of mind.

Ready to Take the Next Step?

Buying your first home involves much more than securing finance. Understanding affordability, government incentives, contracts, legal obligations and project timelines all play a huge part in helping you make informed decisions and avoid the common pitfalls in the purchasing journey.

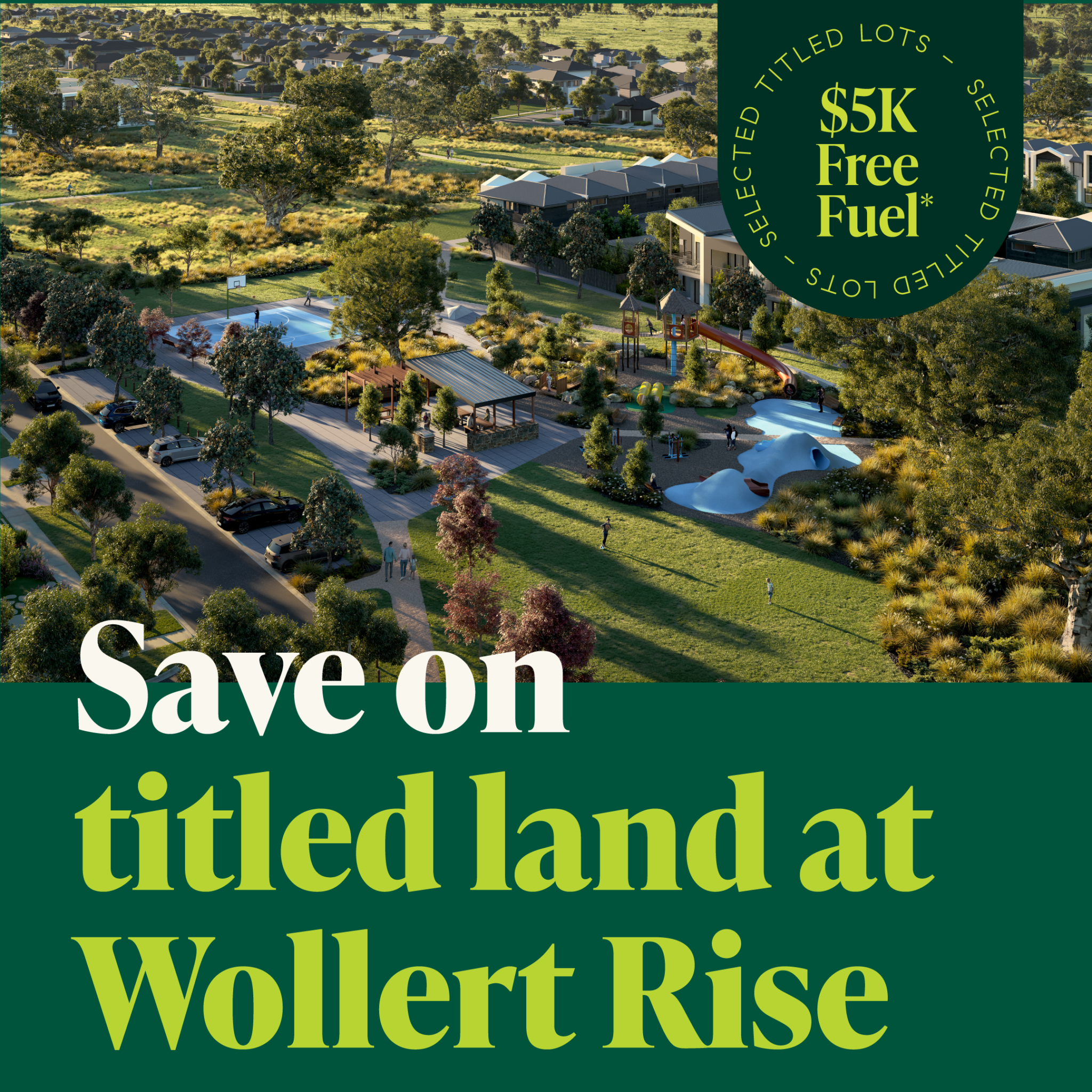

Wollert Rise is a masterplanned community in Melbourne’s thriving north, designed with first home buyers in mind. Residents enjoy easy access to a range of amenities, from the best schools, transport connections, shopping and recreation options, with more on the way as the estate continues to grow.

If you’d like to learn more or chat about the current land opportunities and buyer incentives available, we’d love to hear from you. Click here to contact us: https://wollertrise.com.au/contact/.

Latest updates.

Register your interest.

"*" indicates required fields